KYC and AML Software: What Are the Differences and How Do They Complement Each Other?

Understand the differences between KYC and AML, their importance in regulatory compliance and how to implement effective (and free) solutions for your company.

Key takeaways

KYC and AML are related but distinct processes in regulatory compliance.

KYC focuses on identity verification, while AML deals with preventing money laundering and terrorist financing.

Non-compliance with KYC and AML regulations can result in severe penalties and reputational damage.

Implementing robust KYC and AML software is crucial for businesses to ensure compliance and protect their operations.

You've probably heard about KYC and AML thousands of times, but do you really know what these acronyms mean? Are they the same? Are there differences between them? In the complex world of regulatory compliance and money laundering prevention, these terms are frequently used and mentioned. However, they're not always clearly explained.

If your company is a fintech or belongs to the banking industry, it surely must comply with these regulations linked to identity verification and money laundering prevention. But are KYC and AML the same? No.

Although it's true that identity verification (KYC) and anti-money laundering (AML) are closely related, each concept has a distinct purpose. While KYC (Know Your Customer) is a process that focuses on verifying people's identities, AML (Anti-Money Laundering) regulations go a step further, ensuring that the money handled by these verified individuals doesn't come from illegal activities or is used for terrorist financing. However, both are vital for regulatory compliance, protecting your business, and maintaining your customers' trust.

What is KYC, What is AML, and Their Differences

Know Your Customer (KYC)

KYC (Know Your Customer) is defined as the process companies follow to verify a customer's identity. It can be understood as an introduction, that is, a step prior to initiating a business relationship between both parties.

This process usually has two pillars:

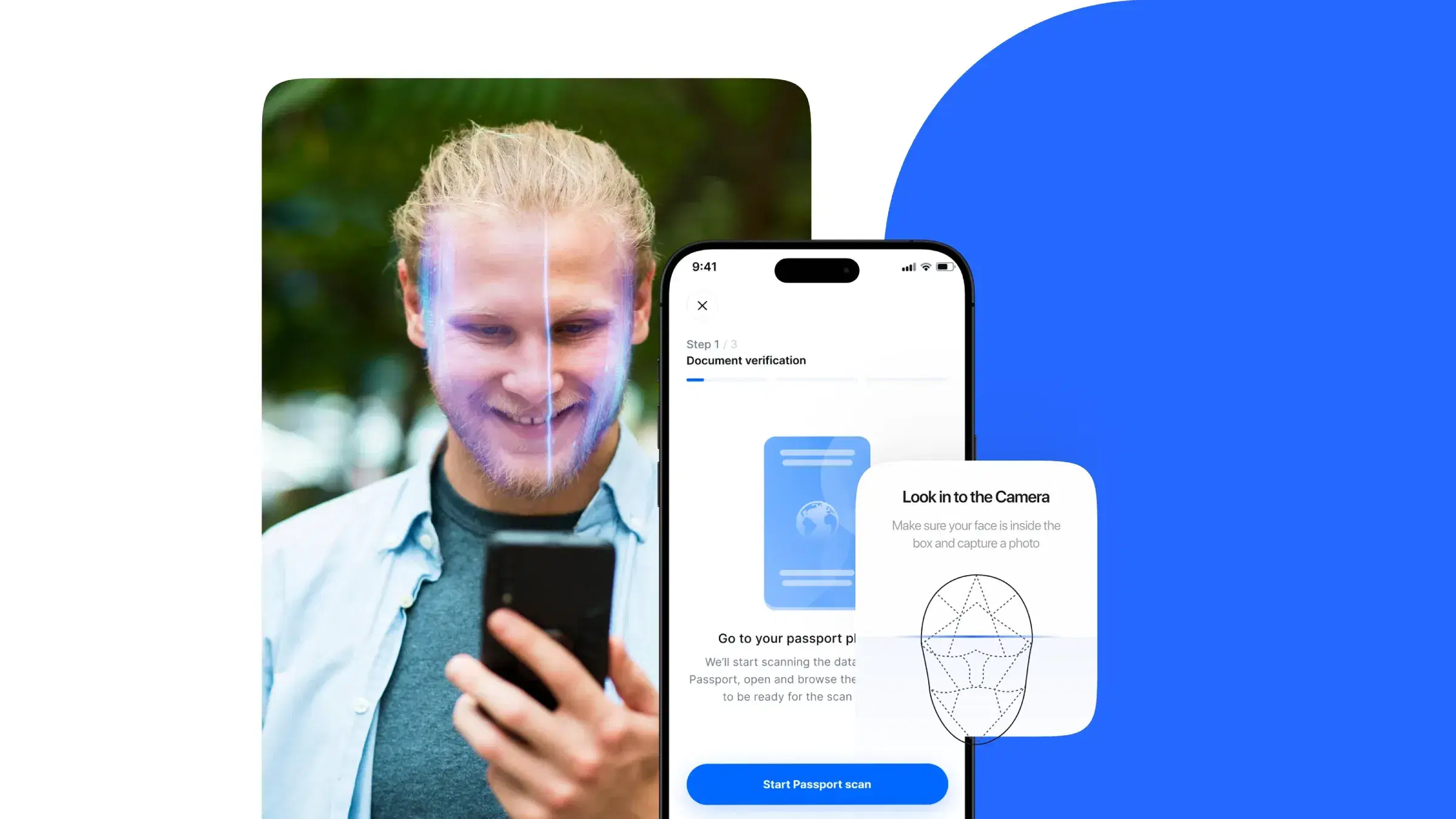

- Document verification. This step ensures the document's authenticity, avoiding frauds such as documentation created by artificial intelligence, and extracts the necessary information to validate identity.

- Facial recognition. This step ensures that the person trying to verify is really who they claim to be, comparing the person's face with the photo appearing on the documentation through facial biometrics. This way, frauds like deepfakes are avoided.

Anti-Money Laundering (AML)

On the other hand, AML (Anti-Money Laundering) is defined as the process by which companies ensure that previously verified identities comply with regulations related to the prevention of money laundering or terrorist financing.

The Differences Between KYC and AML

Thus, once we've defined what identity verification (KYC) and money laundering prevention (AML) processes are, we can understand that the main difference between them lies in the object of analysis: while KYC focuses on verifying people's identities, AML analyzes all those suspicious activities that could be linked to money laundering from illicit activities.

In this way, identity verification (KYC) can be understood as the first phase of a continuous process such as money laundering prevention (AML).

Consequences of Not Complying with KYC and AML Regulations

Complying with KYC and AML regulations is crucial for all companies that must adhere to these regulations. Failure to do so can lead to serious consequences, such as economic sanctions or license withdrawals. In summary, failing to comply with identity verification (KYC) and money laundering prevention (AML) regulations can result in:

- Economic sanctions: Regulators can impose significant fines on companies that don't comply with KYC and AML directives. These sanctions can reach millions of dollars, depending on the infraction's severity. One of the most recent cases is that of TD Bank, one of Canada's most important banks, whose story you can read here.

- Reputational damage: Companies involved in scandals related to money laundering or terrorist financing can suffer serious damage to their reputation, something difficult to quantify. This can lead to the loss of customers, business partners, and investors.

- Legal liability: In some cases, executives of companies that don't comply with KYC and AML regulations may face legal liabilities, including prison sentences.

- Impact on operations: Companies that don't comply with regulations may see their operations restricted, such as the ability to open new accounts or process transactions, until compliance issues are resolved.

Thus, the best solution for regulatory compliance is to implement KYC software and AML software that guarantee companies the necessary protection.

What is KYC Software (Know Your Customer)

All the technology that helps companies complete customer identity verification processes is what we call KYC (Know Your Customer) software. These are tools that help organizations collect, verify, and store user data efficiently, quickly, securely, and in accordance with current regulations.

What functionalities should KYC software include? First, these tools must have sufficient technology to validate and verify the documentation presented by individuals, so as to discard those identifications that raise suspicions due to their inconsistency. These identity verification systems must also faithfully extract the information stored in the documentation.

For its part, good KYC software must include facial recognition. Biometrics has become fundamental due to the rise of deepfakes, so identifying this fraud and allowing the verification of legitimate people is something that should not be missing.

And, in addition to all these features, KYC software should allow companies to know the status of all their users' identity verification processes. Because a good identity verification system is key to effective onboarding.

KYC Software Can Automate the Verification Process

One of the main benefits of KYC software is the automation of identity verification processes. This automation can significantly reduce or even eliminate manual intervention in this procedure. By automating KYC processes, companies can achieve a much safer, more convenient process with an improved user experience.

Moreover, this automation of identity verification helps optimize operational costs, allowing companies to allocate resources to enhance other processes within the organization.

What is AML Software (Anti-Money Laundering)

AML software refers to technology that helps companies execute regulations against money laundering prevention. These tools begin to function once identity verification has been carried out correctly, and are responsible for monitoring transactions that are carried out, checking databases for PEPs (Politically Exposed Persons) and sanctions, as well as alerting to suspicious activities.

Conclusion: AML and KYC Are Different but Complementary

In conclusion, while it's true that the concepts of identity verification and KYC (Know Your Customer) and money laundering prevention (AML, Anti-Money Laundering) are often mentioned together and are related, they refer to distinct processes:

- KYC specifically focuses on verifying customers' identities, ensuring they are who they claim to be. It's the first essential step to prevent fraud and comply with regulations.

- AML, on the other hand, encompasses a broad set of policies and procedures designed to combat money laundering and terrorist financing. It includes continuous transaction monitoring and detection of suspicious activities.

Therefore, KYC can be considered a key component within the overall AML framework. Both are vital for companies, especially in regulated industries like financial services, to protect their integrity and reputation.

If you're looking for an identity verification and KYC solution, at Didit we offer our technology for free, unlimited, and forever. Click on the banner below and contact our team! They will explain everything to you.

Related articles

- Didit Closes $7.5M Seed to Build the Infrastructure for Identity and Fraud

- Non-Document Verification in Singapore: MyInfo-Based KYC Without Document Uploads

- Non-Document Verification in Canada: Credit Bureau-Based KYC Without Document Uploads

- Non-Document Verification in the United States: SSN-Based KYC Without Document Uploads

- Non-Document Verification in France: KYC Without Document Uploads

- Non-Document Verification in Norway: Identity Checks via BankID and Folkeregisteret